Gli sviluppi del commercio internazionale e i possibili scenari post pandemici

The economic benefits of trade are nowadays widely recognized: from much higher levels of production of goods and services, to more efficient use of labor and resources and to the creation of new higher-paying jobs and greater consumer purchasing power. These notions have been paralleled with the assumption that such growth was strictly connected to increasing globalization and consequently higher levels of trade liberalization. However, the impasse into which the multilateral negotiations of the Doha Round have fallen has highlighted the challenges the World Trade Organization is facing, and inherently also the hardships presented for what it represents: trade multilateralism*.

In this forum, for more than a decade, two sides confronted each other on many issues and proved unable to find an agreement:

* On one side, developed nations led by the European Union (EU), the United States (US), Canada, and Japan

* on the other side, the major developing countries, led and represented mainly by India, Brazil, China, and South Africa did not manage to find a common ground on three disputed subjects:

1) the reform of agricultural subsidies,

2) a balance between new liberalizations in the global economy (concerning mainly services and public procurement)

3) the need for sustainable economic growth in developing countries,

4) the improvement of developing countries’ exports access to global markets.

As a result, the 9th WTO Ministerial Conference, held in Bali, Indonesia, from 3 to 7 December 2013 resulted in a Trade Facilitation Agreement that improved customs procedures in order to make it easier and cheaper to trade and made rules more transparent. The foreseen benefits of a 1% cut of global trade costs were expected to translate in an increased world-wide income of more than $40 billion and 65 per cent was of this sum was estimated to go to developing countries. However, the path to this agreement was so long and full of challenges, that all parties welcomed it lukewarmly. So complicated was its process and so lukewarm the support from both groups of countries that it raised doubts over the future of globalization, and the developments of general liberalization in a world where the developing world has been gaining geopolitical power and regional trade blocs have been surging whilst the yearly increase of trade volumes had begun to falter and the aftermath of the Great Recession of 2008-09 was still severely felt. While it is impossible to predict if regionalism will pose an end to multilateralism ad if it will reverse globalization, it is clear that trade is changing nature, mixing multilateral, bilateral and regional trade agreements (RTA).

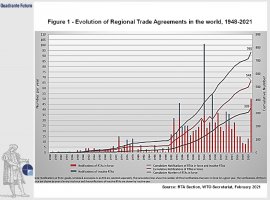

Regionalism surge: Over around the past 7 decades of the WTO existence, RTA has known a steady increase in the number of notifications (Figure 1). As of the 1st of February, 339 RTAs were in force, which corresponds to 548 notifications from WTO members, counting goods, services, and accessions separately.

The most important recent developments in terms of RTA are the following four agreements:

Comprehensive and Progressive Trans-Pacific Partnership (CPTPP) is the successor of the Trans-Pacific Partnership (TPP), which never entered into force due to the withdrawal of the United States as soon as Trump got elected in 2016. To date, it includes 11 parties, Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, and Vietnam. However, future enlargements are expected: on the 1st of February of this year, the UK has formally applied to become a member, the US since in 2018 ex-President Trump had declared his country could have considered joining in the future if some conditions would have been changed, Taiwan who had already expressed interest in joining the TPP and has reinstated its willingness to join and China who announced its desire to join in 2020. Considering that at the time when the signing took place, the economies of the signatories represented, combined, 13.4 percent of the global gross domestic product (approximately US$13.5 trillion), the CPTPP is the third-largest free-trade area in the world by GDP.

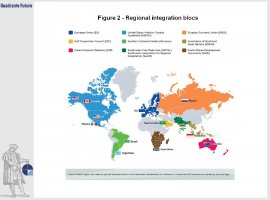

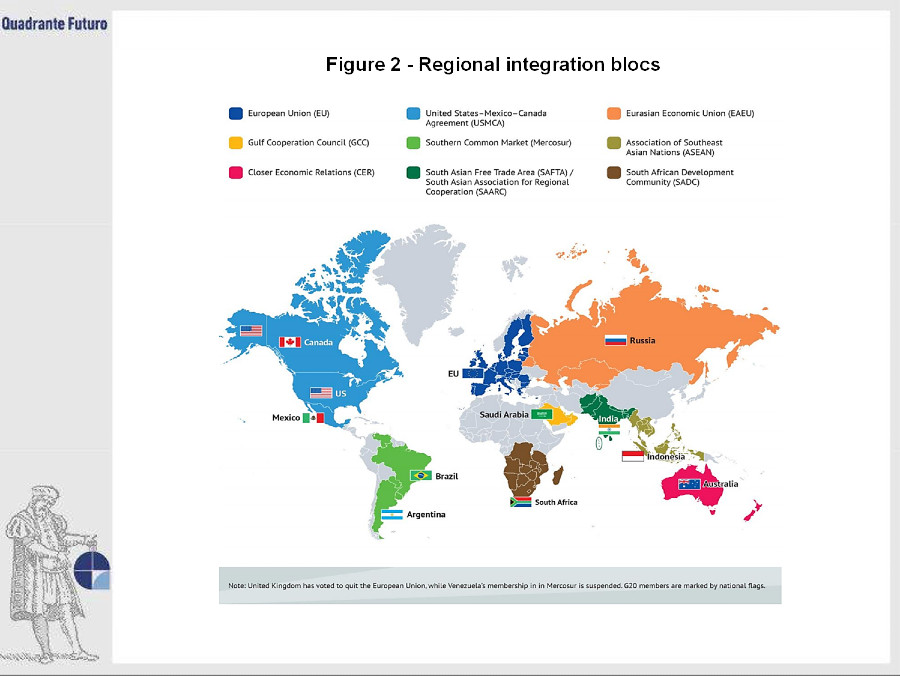

The Regional Comprehensive Economic Partnership (RCEP) is a free trade agreement between the Asia-Pacific nations of Australia, Brunei, Cambodia, China, Indonesia, Japan, Laos, Malaysia, Myanmar, New Zealand, the Philippines, Singapore, South Korea, Thailand, and Vietnam. It was signed on the 15th of November 2020 at a virtual Summit hosted by Vietnam and it unifies 10 ASEAN members and five of its major trade partners. As of 2020, the 15 member countries account for about 30% of the world's population (2.2 billion people) and 30% of global GDP ($26.2 trillion) as of 2020, making it the biggest trade bloc in history (Figure 2). This is an agreement that was conceived already in 2011 at an ASEAN Summit in Bali, and it is expected to eliminate about 90% of the tariffs on imports between its signatories within 20 years of coming into force and establish common rules for e-commerce, trade, and intellectual property. The unified rules of origin will help facilitate international supply chains and reduce export costs throughout the bloc. The RCEP is the first free trade agreement between China, Indonesia, Japan, and South Korea, which are four of the five largest economies in Asia. Much speculation has been made around the trade power China gains at the detriment of the USA and much criticism produced over the alleged ignorance of labor, human rights, and environmental sustainability issues.

The Pacific Alliance between Chile, Colombia, Mexico, and Peru has the potential to become Latin America’s largest economic and trade bloc since its member countries are the eighth largest economy in the world, they make up 38% of the GDP in Latin America, 50% of the total trade and 45% of all FDI to the region. This undertaking has attracted several countries, 52 countries have joined the alliance as observers and associate members. Not only, the PA has announced the start of negotiations with four future associates, Australia, Canada, New Zealand, and Singapore, at the Summit held in Cali, Colombia in 2017. This poses doubts about how it will position itself compared to the CPTPP and the RCEP and what the interplay of these regional agreements in the Asia-Pacific will play ou

The African Continental Free Trade Agreement (AfCFTA) is set to become the world’s largest free trade area since the formation of the WTO, with a market coverage of 1.2 billion people and a GDP of $2.5 trillion, across all 55 member States of the African Union. This is also likely to be one of the most dynamic markets in view of the fact that it is predicted that the continent’s population will reach 2.5 billion by 2050, which will account for the 26% of the projected working world population at that point. The African economy is estimated to grow twice as fast as the one of the developed world. The aim of the AfCFTA is to lower barriers to intra-African trade by making it way easier for African businesses to really ride the growth of the continent’s market. Something, difficult to implement until now, where the average tariffs of 6.1% signified that tariffs where higher within Africa compared to trade outside the continent. ECA estimates that AfCFTA has the potential both to boost intra-African trade by 3 per cent by eliminating import duties, and to double this trade if non-tariff barriers are also reduced.

In light of these developments in the trade arena, two main scenarios are expected to play out:

1) increasing trade regionalism will have a trade diverting role by limiting greater trade liberalization, ,

2) a trade creating situation in which further regional trade integration will reinforce trade liberalization at a greater level.

What is clear is that this is an arena where countries increasingly assert their power.

Please note: mention should be made of bilateral trade agreements between China and many developing countries, mainly in Africa and South America.

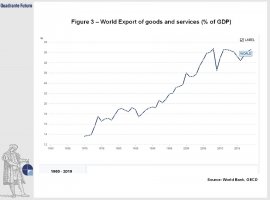

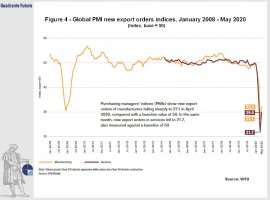

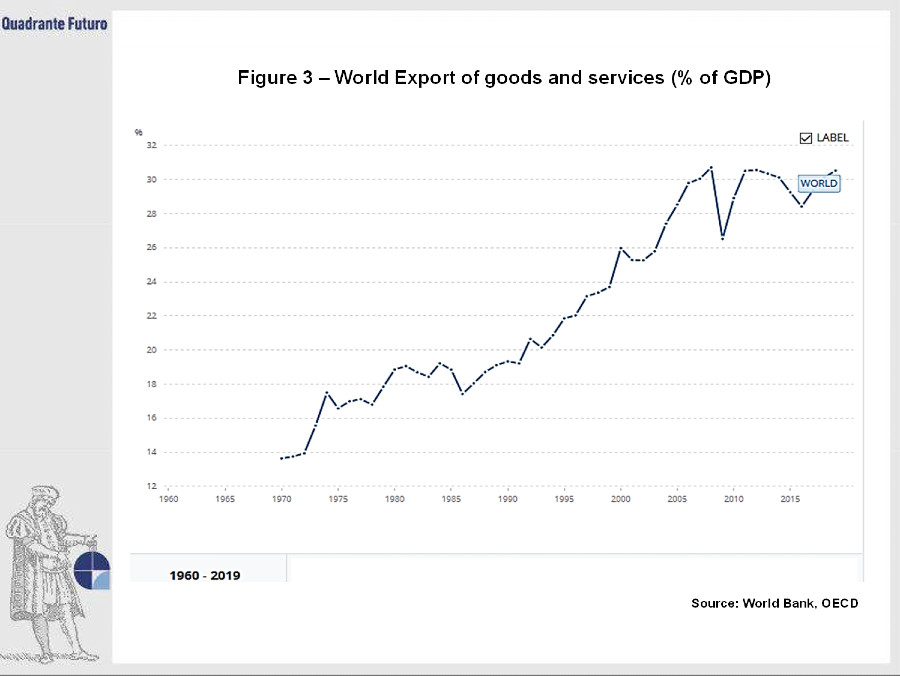

Further, mention must be made in the text of the slowdown of international trade as a consequence of the financial crisis (Figure 3 and Figure 4)

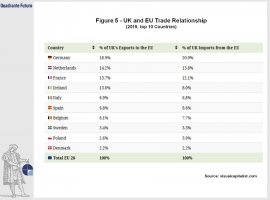

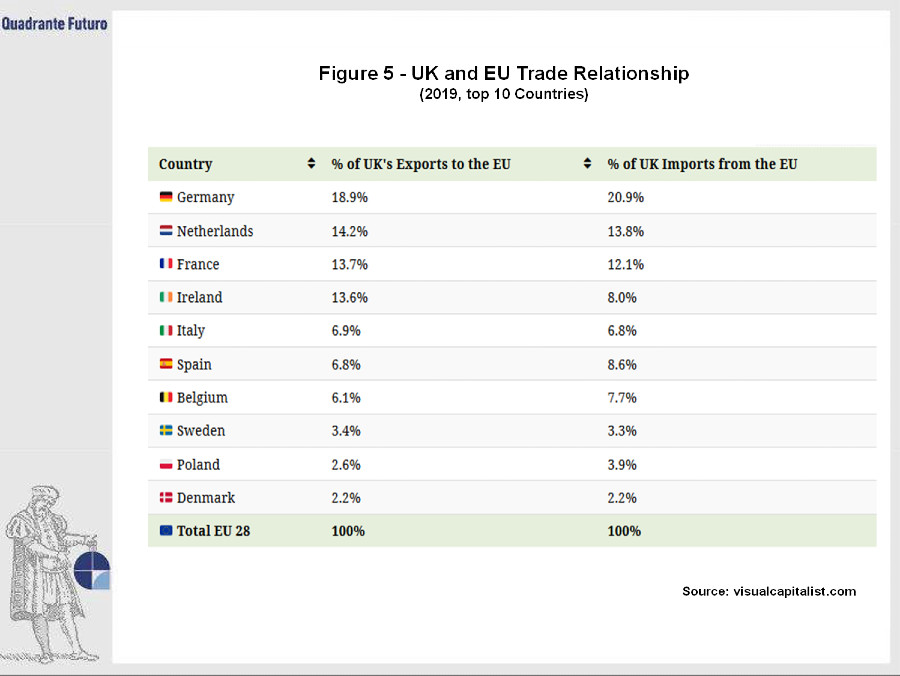

Finally, a reference should also be made to Brexit and fears that UK-EU trade will collapse (Figure 5); as well as to the sudden increase of political-economic tension between the new democratic dministration under President Biden and Russia and to the stormy meeting between Chinese and US officials in Alaska a few days ago.

It would seem to me that the vision of a world united by trade would continue to remain … a vision. However the world is probably not going to revert to the “closed borders” situation of the Thirties. Some markets, like the oil market simply have to remain open.

* In general, "trade multilateralism" is the definition of any trading system based on trade agreements among three or more nations that are aimed at reducing tariffs and at making it easier for businesses to import and export. In this article, trade multilateralism is embodied by the World Trade Organization (WTO) which, to date, has over 160 members and it represents 98 percent of world trade.

© Riproduzione riservata

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}