Lo sfruttamento dei giacimenti di minerali ferrosi in Guinea potrebbe far diventare questo piccolo paese uno dei primi produttori al mondo nel settore

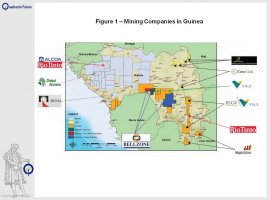

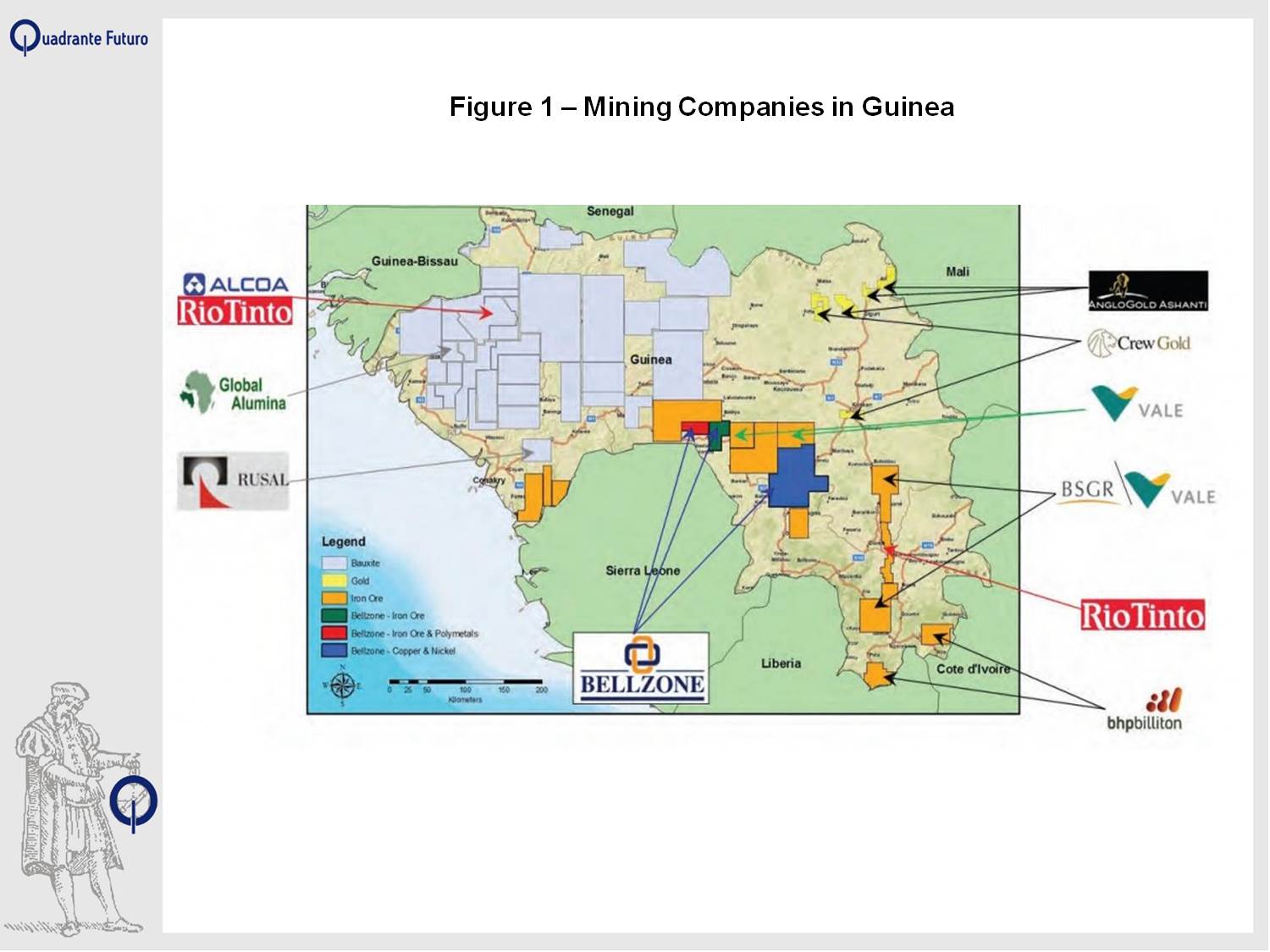

Guinea, a small resource rich country in the hearth of Western Africa, is at a critical juncture. The country has recently struck a deal worth $20 billion with Rio Tinto, a British-Australian metals and mining giant, to exploit the part of Simandou, one of the world's biggest deposits of iron ore on the Eastern part of the country

(Figure 1).

Estimated at around 2.2 billion tonnes, the concession contains almost as much as the entire global iron-ore industry produced in 2013. The new deal should enable the company to mine 95m tonnes of ore every year, turning the small country in one of the top producer of iron ore, as well as doubling the West African state's GDP. Rio Tinto has also agreed to build a deep-water port and a railway line to take the ore 650km (400 miles) to the sea. Guinea's government hopes it will create a "growth corridor" stretching the length of the country. Just across the border in Sierra Leone, new iron ore operations was responsible for the largest hike of GDP in the history of the country, with a 15 % growth recorded in 2012 followed by a 16% in 2013, which made it one of the fastest growing economy in the world according to the IMF.

The new bonanza represents both a clear opportunity but also a threat. The key challenge faced by Africa's resource-rich countries consists of transforming the resources in the ground into assets that lead to strong sustainable growth, economic diversification, reduction of inequality and poverty, and equity between generations. Geographical or climate variables seem not to explain why states perform badly and, even after controlling for trends in commodity prices, those countries seem to fail in natural resource-led development.

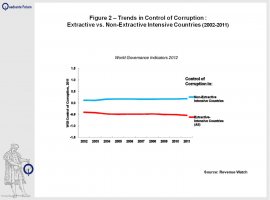

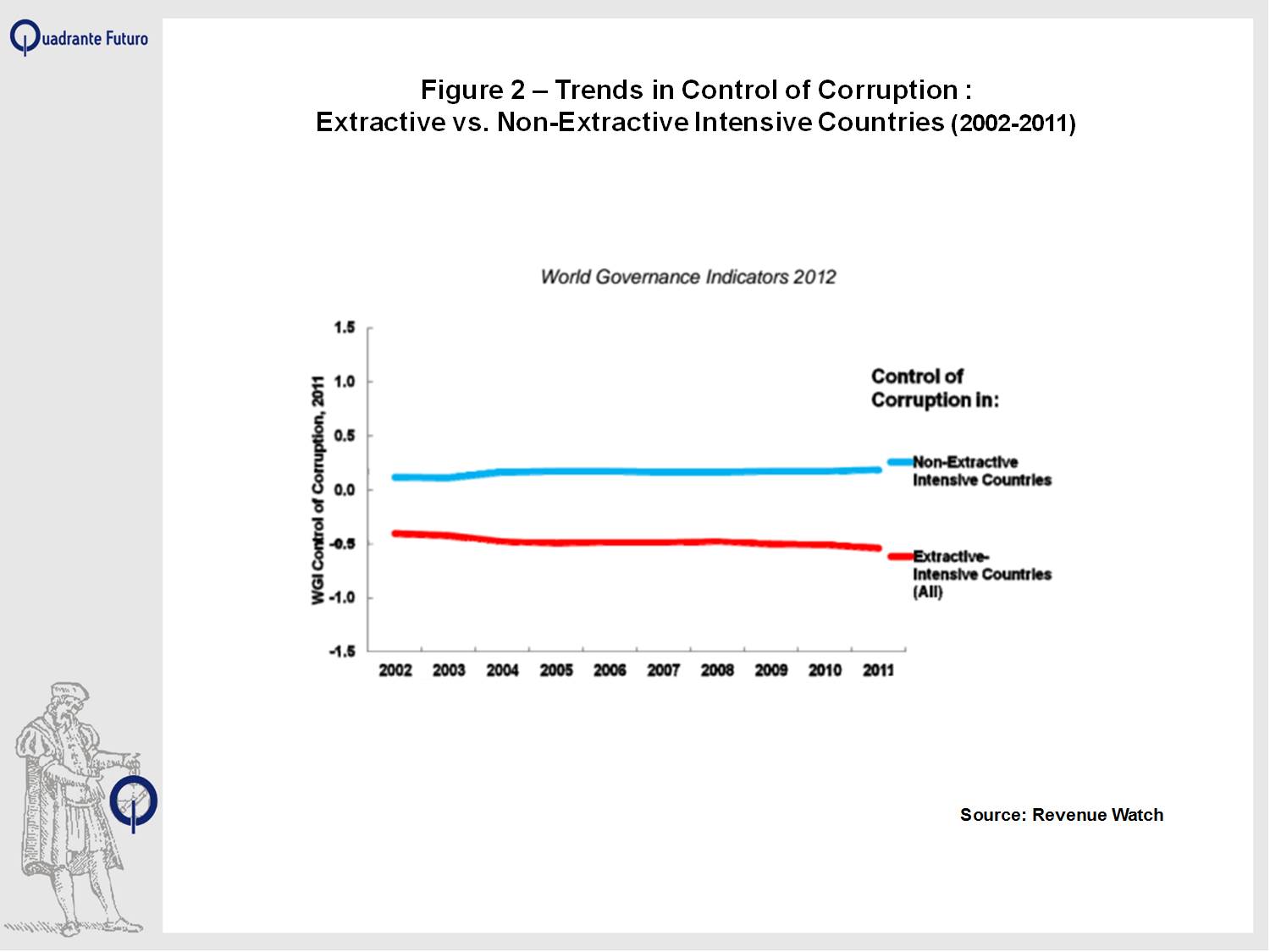

Positive wealth shocks from the natural resource sector creates an high demand for non-traded products and drives up non-traded production and prices, including particularly input costs and wages. Conversely, profits in traded activities such as manufacturing often suffer due to the country's currency appreciation, which makes import cheaper and export more expensive (a phenomenon commonly known as Dutch disease) Consequently, the decline in manufacturing and agro processing may undermine the growth process. An other major risk is related to the political process: government officials in such countries are tempted into rent-seeking and possible corruption (Figure 2) rather than pro-growth activities; on the other side there is evidence that resource richness is related with more authoritarianism but, unfortunately only weak evidence for an link between non-authoritarian political systems and growth.[1]

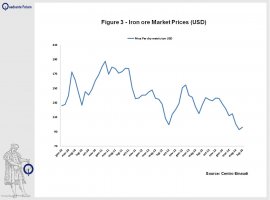

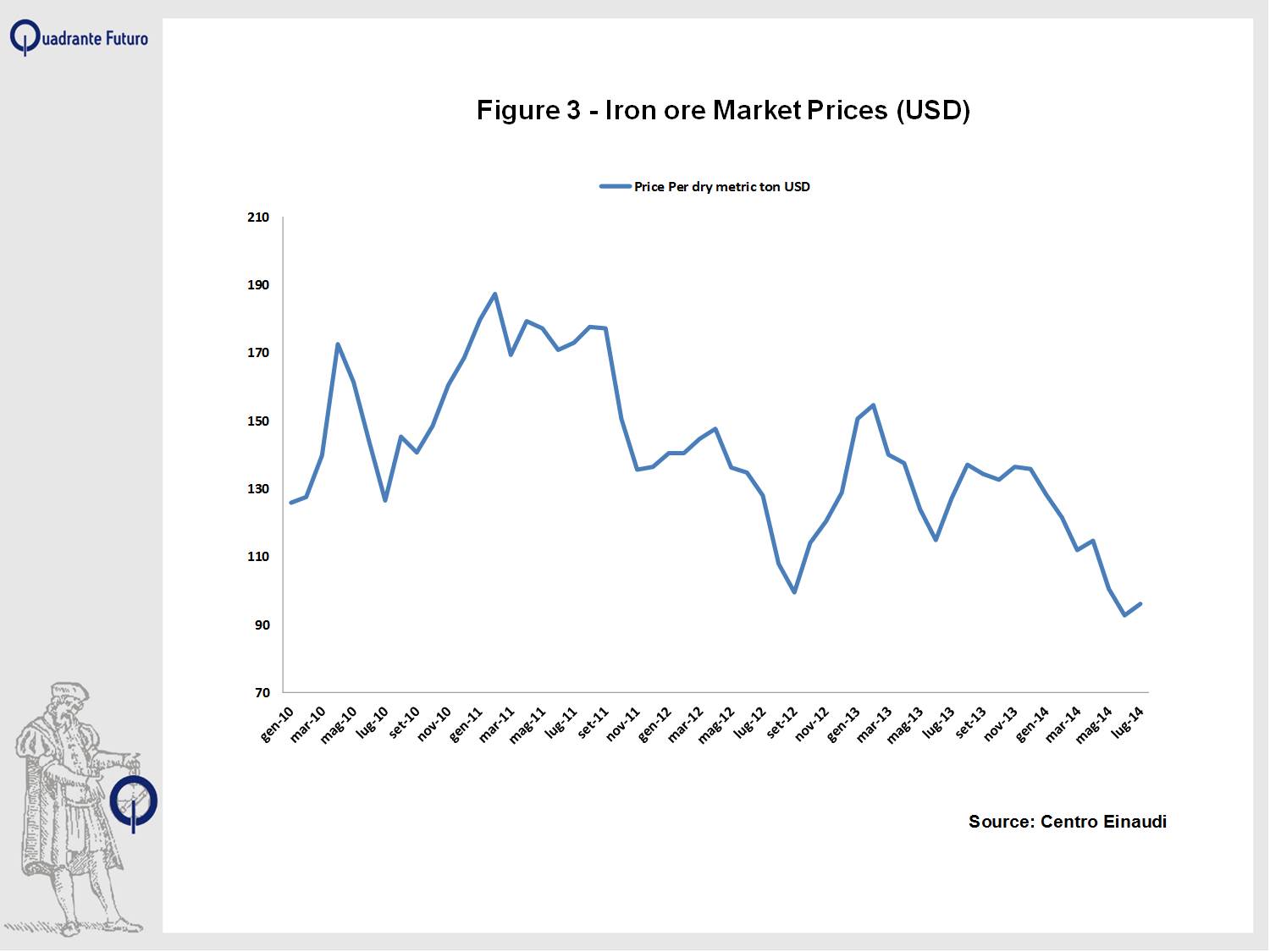

But the most pressing challenges may be faced by the possible sudden end of the rush to produce and export iron ore, which have experienced a sharp decline in the past 3 years.

Iron ore prices have toppled from nearly 200 USD per Ton in 2011 to around 80 USD in the recent months (Figure 3), and most investors are betting on further declines.

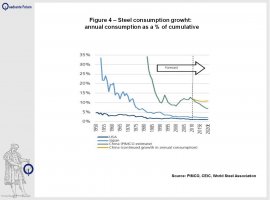

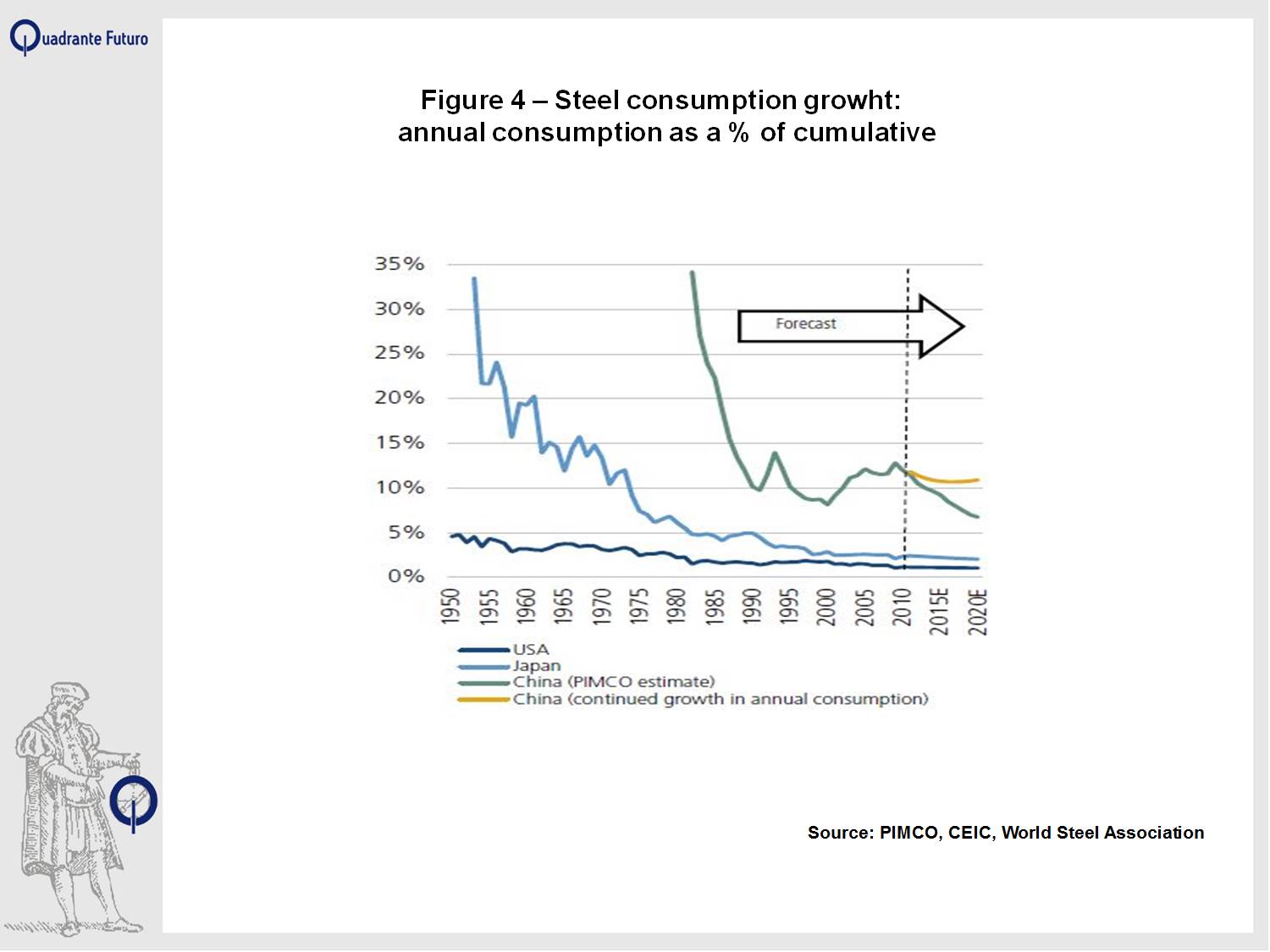

The cooling off of the demand of steel in China, which consumes two thirds of global ore supply and makes nearly half of the world steel, is one of the major reasons behind this drop (Figure 4).

The other driving force is the dramatic rise of supply. UBS predicts the seaborne market will be awash with almost 74 million tons of surplus iron ore this year. By 2016, the seaborne market could be oversupplied by 267 million tons—or as much as Rio Tinto, the world's No. 2 iron-ore exporter, produced last year.

For big operations like Simandou, which claims to be extracting one of the most valuable quality of iron ore, production remains highly profitable. Yet this may not be the case for smaller producers with reduced economies of scale and exploiting lower quality iron ore.

A further uncertainty has been generated by the most recent outbreak of Ebola which is affecting the core of the new iron ore boom. While Ebola does not seem to have affected major producer, it risks adding further uncertainty on smaller producers who are already been affected by the above mentioned drop of prices.

Despite the uncertainty of the future of iron ore production, both Guinea and Sierra Leone are facing a real euphoria, which has only been halted by the current Ebola emergency.

Once this is over and the countries get back on track, Governments may be tempted to incur in expenditures which may not prove sustainable in the medium term, particularly if the boom does not materialize as expected .

The most recent experience of Ghana, whose euphoria generated by oil discovery has translated into a doubling its public debt in the past 7 years should serve as a warning for both countries.

The case of Botswana, which has managed to turn the diamond wealth into impressive economic and social outcome thanks to a strong policy of diversification and quality of spending, can also provide a number of more positive lessons.

[1] The curse of natural resources, Jeffrey D. Sachs, Andrew M. Warner

© Riproduzione riservata

{kind=link}

{kind=link}

{kind=link}

{kind=link}