I Green Bond favoriscono gli investimenti in progetti che portino benefici ambientali e, pur essendo strumenti finanziari relativamente nuovi, stanno registrando una crescita straordinaria

At the 2015 COP21 in Paris, 188 delegations presented plans of their countries to try to maintain a rise in global temperature below 2 degrees Celsius this century. Institutional investors, representing $11.2tn, pledged to increase investment in climate-aligned assets and to support the growth of a green bonds market. Green bonds enable capital-raising and investment in new and existing projects with environmental benefits. Like all other bonds, green bonds pricing proceed is identical to that of ordinary bonds, their green label however requires them to be linked to projects that have a positive impact on the environment, e.g. energy efficiency, energy production from clean sources, or sustainable use of land.

What is a Green Bond?

Green bonds are designed to have positive environmental impact. Their value resides in the fact that the issuer pledges to use the funds raised to finance projects having a positive impact on the environment. This signifies a commitment to exclusively use the funds raised to finance or re-finance “green” projects, assets or business activities (ICMA, 2015). While conventional bonds can fund all of a corporate’s activities, for a bond to receive a green label it must fund investments linked to the environment. Historically, green bonds have the same risk and same return as conventional bonds. However, there are additional costs associated with the issuance of green bonds, including a disclosure of their use of proceeds.

As already said, green bonds were created to fund projects that have positive environmental and/or climate benefits. Now the majority of bonds are either green project bonds, meaning ring-fenced for the specific underlying green project(s) or green “use of proceeds” bonds, meaning earmarked for green projects. According to the Green Bond Principles (GBP, year 2014 — a set of voluntary guidelines framing the issuance of green bonds), the recognized categories include but are not limited to the following:

● Renewable energy

● Energy efficiency (including efficient buildings)

● Sustainable waste management

● Sustainable land use (including sustainable forestry and agriculture)

● Biodiversity conservation

● Clean transportation

● Sustainable water management (including clean and/or drinking water)

● Climate change adaptation

Green bonds are an innovative solution to encourage corporations to bend their businesses towards sustainable practices. A growing investor base of pension funds, mutual funds, sovereign funds and other institutional investors, who have either created green specific funds or have a green mandate, can generate a large, liquid and diverse source of demand. This pool of buyers has started to push for new issuances in larger lot sizes and higher volumes. This jump in demand creates incentives for corporates to tie specific green projects to green bond financings.

They make it possible for investors to directly trace money raised for specific green business activities. This gives green bonds both a financial and environmental impact (Figure 1).

Independent review and oversight

Generally, green bond issuers are subjected to legal documentation and must specify that the funds will be used to finance or refinance projects with environmental benefits. A green bond should not be confused with already existing sustainability bonds, which are conventional bonds with an ESG (Environmental, Social and Governance ) rating from a rating agency.

Second-party reviews and consultation are frequent. Companies like Sustainalytics, Vigeo EIRIS and Oekom commonly provide external review for green bonds issued by banks and U.S. municipalities. CICERO, another second-party reviewer, offers a “Shades of Green” methodology whereby green bonds are graded “dark, medium or light” green depending on the underlying project’s contribution to “implementing a 2050 climate solution” (Clapp and Torvanger, 2015).

Moreover, green bond issuers are required to report regularly on the use of funds and they are encouraged to have independent verification via audits of certain aspects of the green bond process, such as the internal tracking method and the allocation of funds from proceeds. Third-party certifications by NGOs or other organizations are in use or in development. The most influential is without doubt the Climate Bond Initiative, an international, investor-focused not-for-profit working solely on mobilising the $100 trillion bond market for climate change solutions.

While nominally many types of corporations could qualify to issue a green bond, many are eliminated simply because of a lack of transparency.

In 2016, China was the domicile for the majority of green bonds issuance. Chinese regulators have begun developing a China-specific “Green Bond Guidelines” with unique standards of review and verification. The standards, part of a broader green financial reform initiative, are designed to guide corporations and other market participants. While the standards are expected to be different from those generally followed by western issuers, reviewers and NGOs, climate change advocates are supportive of the China specific reforms

Market Volume

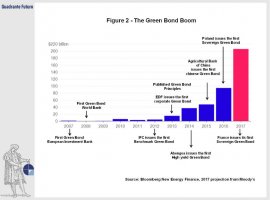

The capital markets can play an important role in mobilising private funding for climate change mitigation and adaptation projects. Although Green Bonds are relatively new financial instruments, they have experienced extraordinary growth since 2007 (Figure 2) with the market really starting to take off in 2015 when $42 billion was issued; almost four times the 2013 issuance of $11 billion. 2016 issuance was double 2015 with [$80bn] issued and with $53 billion issued to date, in 2017, there is the potential that as much as $130 billion is issued by the end of the year. With continued strong issuance momentum, and c. $200 billion in green bonds currently outstanding, liquidity is at a level that many institutional investors are taking notice.

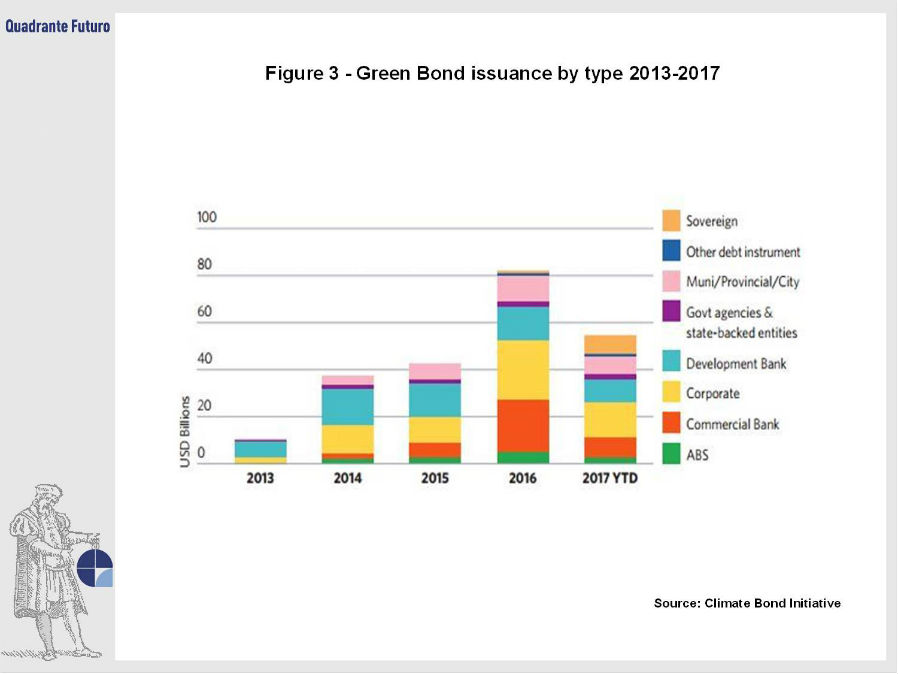

This robust expansion now provides access to a market that is diversified in terms of issuers, geographical coverage, currencies and ratings (Figure 3). Continued diversification can further strengthen the sustainability of the market. Additional issuance should establish more bonds with a wide array of ratings (both Investment Grade and High Yield. The market is expected to attract more North-American and Asian issuers, with China’s reforms being a key driver. The very successful first sovereign issuers, Poland and France (in 2017), are expected to foster additional activity by other sovereigns. Finally existing issuers are expected to seek funds for refinancing or new projects and space new issuances along the yield curve.

China’s $36 billion of green bonds issued in 2016 (2 percent of China’s bond market) made up more than a third of 2016 green issuance. The world’s most populous nation may again double issuance in 2017, according to Tracy Cai, the Chief Executive Officer of Beijing-based Syntao Green Finance. Even though the communication between Chinese issuers and the ICMA (International Capital Market Association) has increased in recent years, there is a significant gap between what China considers to be a green bond and what is restricted by the ICMA. For example, in China, green bonds can be used to fund coal power plants, if the project meets certain criteria. Whereas the ICMA understandably rejects green financings of coal projects.

While the growth in the market is very encouraging there is a long way to go to reach the threshold of $53 trillion, that, according to the International Energy Agency (IEA), needs to be invested to keep global temperature increase below 2 degrees celsius before 2035.

History of the Market

When the Green Bond market first developed, multilateral development banks (MDBs) were the primary issuers. MDBs primarily acted as a “conduit” to disburse green allocated funds to new green projects. The logic was that MDBs could act as an established creditworthy issuer with the ability to raise capital for new green projects which may not have had access to attractive financing. The MDBs committed to separate and monitor the disbursed funds with undisbursed capital kept on deposit.

At this early stage of climate finance, projects were relatively short-dated and focused on water management, waste management and sustainable transport as well as renewable energy and energy efficiency

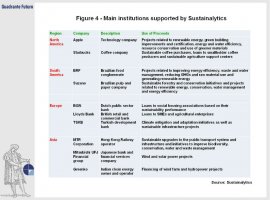

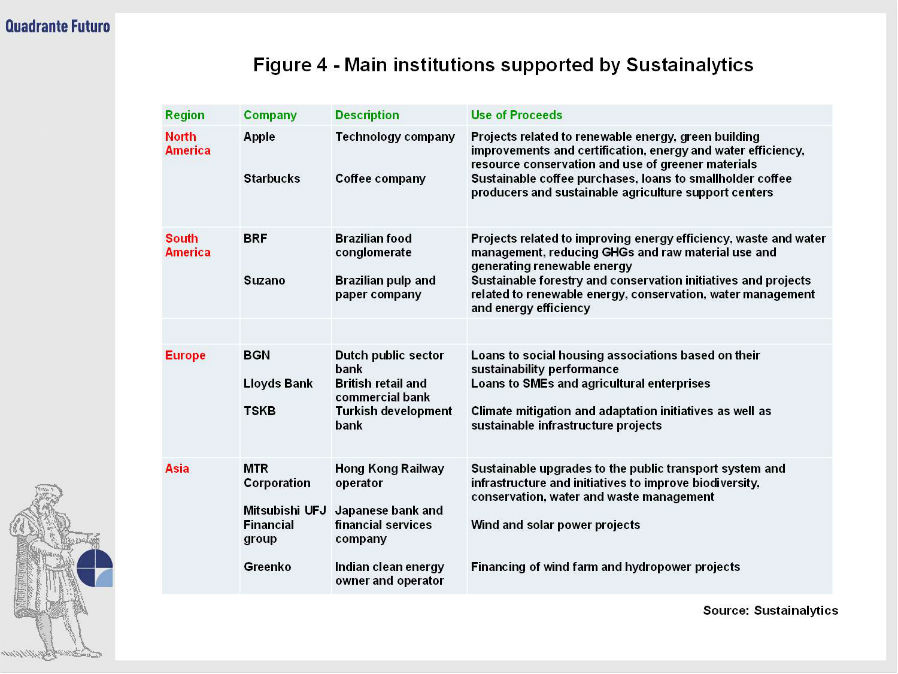

After the financial crisis, companies needed to diversify their investor base and sustainable financing became a way to access new investors (Figure 4). The current trend is to raise green capital to refinance existing assets as well as finance new projects. Besides having to pay a small additional cost for ESG analysis costs and second opinion fees, Green bonds have several advantages for issuers:

1) They are an attractive financial tool that can lower costs of financing

2) They encourage diversification of investor base

3) They attract “the responsible investor” who is known for having a long-term investment profile

4) They are normally of a larger size than conventional bonds with longer maturity

5) They often have a Credit advantage leading to cheaper financing

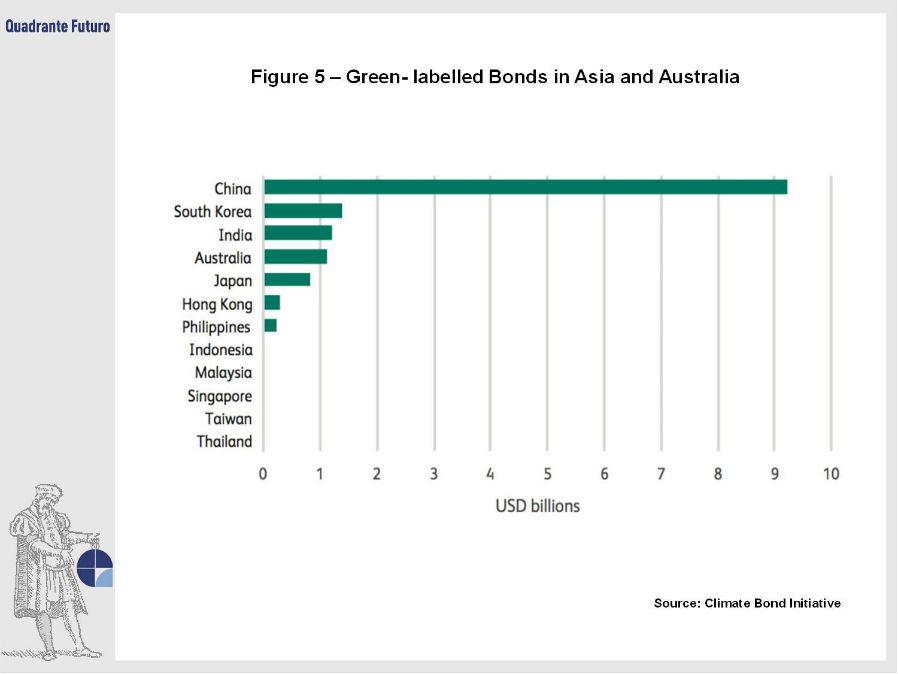

2015 saw an increase in emerging market issuance, given the strong political commitment in many emerging market governments to grow local green bond markets. Issuance in emerging markets (Figure 5) has widened the types of projects financed, with proceeds leveraged to other green sectors, e.g. low carbon transport and water management. Major issuers in China included Goldwind and Agricultural Bank of China and in India included Export-Import Bank of India and IDBI (formerly known as Industrial Development Bank of India).

In 2016 the EBRD European Bank for Reconstruction and Development raised €1.64 billion through 57 bond issues in eight different currencies.

Finally, the Paris Agreement in 2015 opened the way for a new green financing trend: in 2017 for the first time green bonds were issued by governments. Poland, the first ever sovereign to issue a green bond with a EUR 750m bond financing, was followed by France with a $7.4bn issuance in June 2017.

Earlier this year, the Lagos Conference set stage for a Nigerian Sovereign Green Bond, scheduled to be the first sovereign issuance from an African nation. The bond has been provisionally earmarked for a range of climate-related initiatives including mass transit, land reforestation, remediation and solar projects. A series of announcements have been made by other sovereign countries such as Morocco, Sweden and Kenya, all foreshadowing action next year. The Brazilian Development Bank (BNDES) recently announced a 500-million real ($159 million) sustainable energy fund and is seeking to tap the green bond market in the second half of 2017.

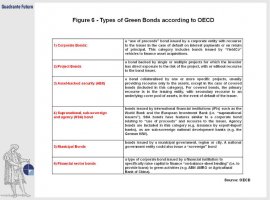

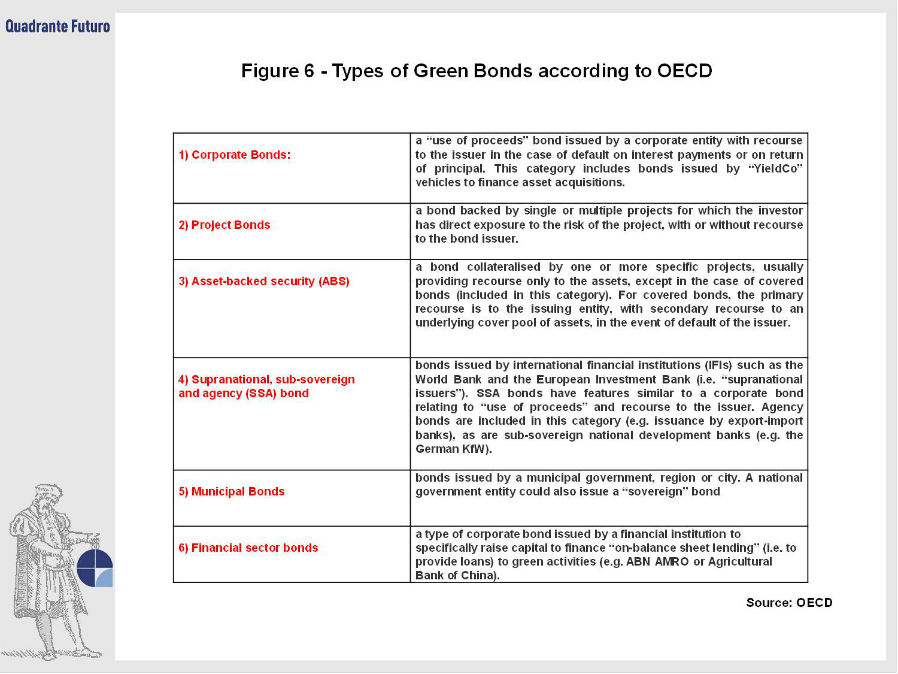

According to OECD there are six types of green bonds (Figure 6).

Issues with self-regulation

While green bonds do appear to offer an effective means of addressing climate concerns, a solid framework still needs to be established to guarantee their credibility. In particular because many green securities are “self-labelled”, meaning that are bonds whose proceeds are used to finance low-carbon and climate-resilient (LCR) industries, sectors and solutions but do not yet carry the green label yet (CBI/HSBC, 2015).

The review mechanism provides a first attempt for green bond standardization. The first level is a second party opinion, the second level is provided by independent accounting firms, the third level is the Climate Bond Initiative (CBI) certification and lastly, a green label can also be applied to a bond by another entity via its inclusion in a green bond index or via a “tag” on analytical tools widely used in financial markets such as the Bloomberg Terminal. Many institutional investors are required to invest exclusively in “benchmark-eligible” securities, so having a green bond included in a benchmark index can be an important attribute for attracting these mainstream investors. Recently, LuxFlag (The Luxembourg Finance Labelling Agency) introduced a green-bond label to eligible investment vehicles. Its objective is to reassure investors that the applicant invests, directly or indirectly, in the Responsible Investment sector. The applicant may be domiciled in any jurisdiction that is subject to a level of national supervision equivalent to that available in European Union countries..

Since March 2014, a number of ratings agencies and financial institutions have created indices to exclusively cover green bonds. In March 2014, Solactive launched the first green bond index, followed in July by S&P with their S&P Green Bond Index and the S&P Green Project Bond Index. Bank of America Merrill Lynch launched their index in October 2014 and finally in November 2014, MSCI collaborated with Barclays to launch family of green bond related indices.

Reflections

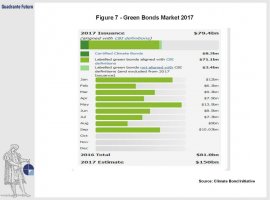

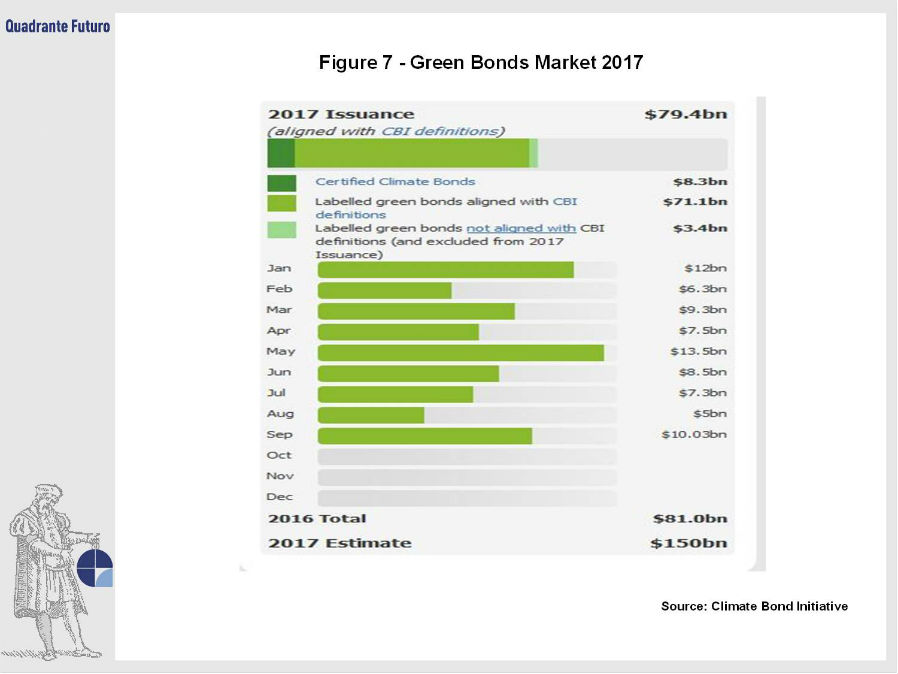

Green bond market observations (Figure 7) reveal that corporate green bonds have New Issue Premium (NIPs) that are equal to those of comparable traditional bonds, indicating that they are accepted by regular market participants. Moreover, even if issuers could fund themselves and their green projects without using a green bond designation, this new green labeled security certainly broadens issuers access to a larger and more diversified investor base. In addition green bond issuance supports corporate reputation around sustainability and creates a new green dynamic mindset in financial markets.

Green bonds encourage investors to include climate considerations as part of the investment process. This change has potential short- and long-term financial market implications but more importantly it is likely to drive longer-term consequences for the society. First, Green bonds have a diversification impact increasing the number of products supplied to financial markets and increasing the number of issuers in the market.

Green bonds have shown that they can be issued at all rating levels and across all sectors from corporates, municipalities, sub-sovereigns and sovereigns. Green bond issuance is agnostic across emerging and developed markets. While Nigeria is preparing to issue its first Sovereign Green Bond, France plans to utilize the proceeds from its green bond issuance in new areas specifically to finance tax credits.

Finally, there is a clear shift in investor types from central banks and official institutions to Assets Managers, Banks and Insurance/ Pension Funds (for example Italy’s current green bond issuers are: Intesa Sanpaolo SpA, Hera SpA, Innovatec SpA, Alperia SpA, ELY SpA, Green Arrow 11 Srl) This is further broadened by a geographic transition across Asia, Scandinavia, Europe, and the USA. This increases the number of investors per deal and reduces the investors ticket sizes.

Still, private investment will continue to be urgently needed to supplement scarce government funds and credit in particular in developing countries. These investment products must be designed to appeal to investors with substantial asset bases on which to draw. Pension funds and sovereign wealth funds have large allocations to fixed income and therefore a strong incentive to finance private green investments, therefore reducing the burden on public credit usage to fund green projects.

© Riproduzione riservata

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}