Il 14 giugno 2018 Mario Draghi ha annunciato la fine del Quantitative Easing, dopo tre anni e nove mesi di attività, Che cosa ha significato questa politica monetaria della BCE per l'area euro?

Thursday, June 14th 2018: the end of the Quantitative Easing has been announced by Mario Draghi, the President of the European Central Bank, at the Riga’s Governing Council. After three years and nine months of activity the program will end in December 20181 . An evaluation of the policy is therefore appropriate at time. What has the ECB monetary easing meant for the Euro Area? Did all the countries react at the same time? For how long will the benefits, if any, last for our economies?

The APP and the long-term effects

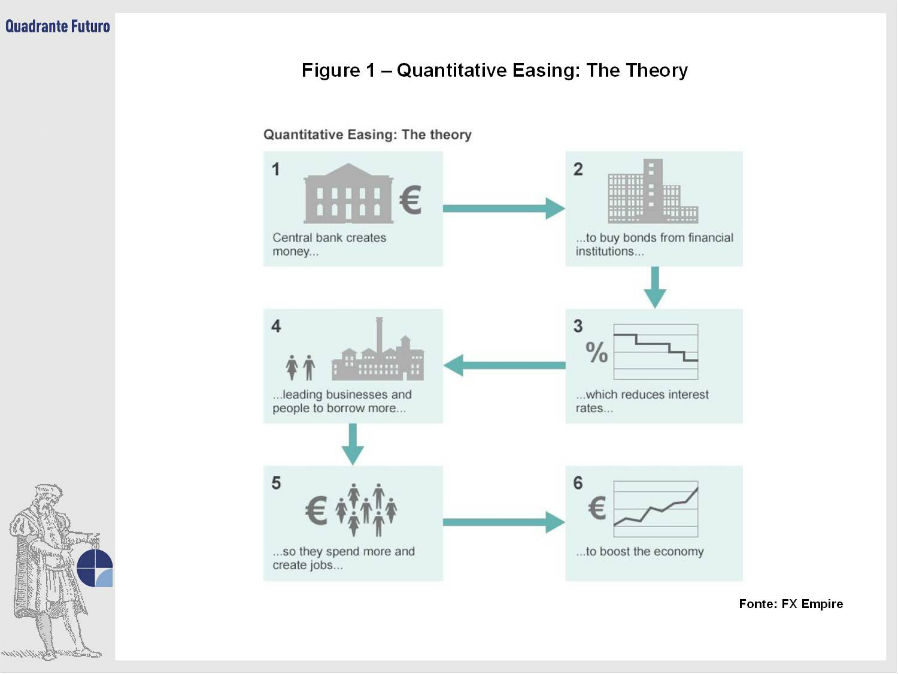

Shortly after the beginning of the financial crisis in the summer of 2007, followed by a global major recession in 2008 and 2009, most central banks intervened aggressively both by cutting interest rates and by adopting a number of unconventional monetary policy measures. The latter included large scale asset purchases, also known as Quantitative Easing (QE - Figure 1), initiated by US Fed in 2008, 2010 and 2012, by the Bank of England in 2009, 2011 and 2012, by the Bank of Japan in 2013 and by the European Central Bank in 2015.

More specifically, on the 22nd of January 2015 Mr. Draghi announced the so-called expanded Asset Purchase Programme (APP), an unprecedented expansionary monetary policy measure aimed at fulfilling the mandate of the ECB. Indeed, after years of very weak inflation rates in the Euro Area, there was a need to step up the efforts to restore price stability, defined as an inflation level below, but close to, 2% in the medium term. After three years since the first implementation of the policy, it is reasonable to assess the macroeconomic effects of the APP on the Euro Area. The reader can rely both on academic and institutional research appraisals and verify that they all converge to the same outcome: the APP has had a positive impact on inflation and GDP growth rate. The ECB estimates an impact of 1.9% (in cumulative terms) on both GDP and inflation growth exclusively due to the operations2 conducted between 2014 and the end of 2017.

Regarding inflation, ECB projections for 2018, 2019 and 2020 are respectively rising from 1.1% in 2018, 1.5% in 2019, 1.8% in 2020. Similarly, the effect at aggregate level on the GDP rate is estimated to be 2.4% in 2018, 1.9% in 2019 and 1.7% in 2020. These numbers reveal the disparity with deflation and null growth we experienced when the program started.

Before the APP. What about the major economies?

Nevertheless, this note aims at describing the response of the major four countries (Germany, France, Italy and Spain) to the policy shock, at its introduction in the first quarter of 2015. Main references of the topic have its origin from the author’s research thesis and the contribution of other economists mainly settled at the ECB and expected to find similarities among the “peripherals” Italy and Spain, as well as between the “core” countries Germany and France.

The inflation trend was relatively homogeneous before the intervention: decreasing or flattening close to zero. GDP dynamics instead followed a different path.

During 2013-14 Germany and France experienced a GDP growth between zero and 2%. Germany enjoyed better economic conditions led by investment growth, a rebound in the labour market and higher confidence from consumers. France on the contrary, was suffering from internal lack of substantial reforms that were responsible for a low and flat, but not negative, growth rate in the late 2010s.

After the economic stabilization of 2013, the Italian economy dampened by decreasing investments. Until the end of 2014 the Italian real GDP growth was slightly weakened due to high idle capacity. Inflation remained close to zero at negative values.

At the end of 2014 the positive trend in Italy regards a slightly higher internal demand and the depreciation of the Euro that favours export competitiveness. Credit supply shrank further, registering a fall of -1.2% of credit easing to Non-Financial-Corporations (NFC) in the private sector, accompanied by a lower demand. The Italian economic picture in the last quarter of 2014 was in line with the Euro Area tendency, and the cyclical situation in the first quarter of 2015 demanded a positive shock able to boost the economy. During 2014 the Spanish economy continued along the recovery path started in mid-2013. The driving factors of the economy were increased confidence of firms and consumers and favourable performance of the labour market, the whole included in a valuable environment of financial conditions. The GDP increase, in 2014, totaled up a remarkable +1.4%.

Aftermaths: why heterogeneity?

Going directly to the results, there are two clear evidences. First, Italy better responded to monetary policy. Second, the expected differentiation among core and peripherals did not emerge. Regarding the former, Italy reacted better to the policy impulse in terms of GDP, inflation on the long term and 10 year-rate in the short one. The business cycle conditions showed above are consistant with this result. Unlike France and Germany, Italy lacked an external incentive to boost the stagnant economy. However, the disparity with Spain was not taking into account the debt growth shared by the two Mediterranean countries. Indeed, the Iberian reaction to the APP in the short as in the long term was lower than the italian and more in line with the french and german response. The reason is to be read via the business cycle key, which was shared by all the countries but Italy. A different picture, even more interesting in a sense, emerges from the pass-through of the monetary policy via the credit channel. The analysis regards volumes and rates to household and NFC. Economics is often (rightly) accused of dealing with obscure matters, unintelligible to most people and incapable of providing an answer to the main real economy issues. Trying to meet this need, the analysis regards how loans to families and firms have been affected via rates and volumes in the past three years thanks to the APP. The apparently puzzling outcome finds its explanations in highly country-specific credit markets under investigation. The textbook suggests a first phase consisting in a reduction of interest rates (swiftly mutable via markets activity) and a second one where the volumes increase. Concerning the first phase, due to already stabilized rate levels, the reduction was contained and quite homogeneous among the four countries. With the volume phase comes the engaging part: Germany and Italy remarkably responded to the crises with a boom in loan volumes, under a counterfactual analysis3 . This is plausible for countries highly dependent from the banking system and economies greedy of liquidity injection.

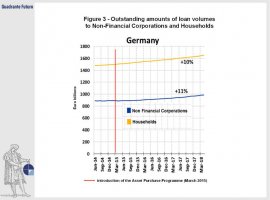

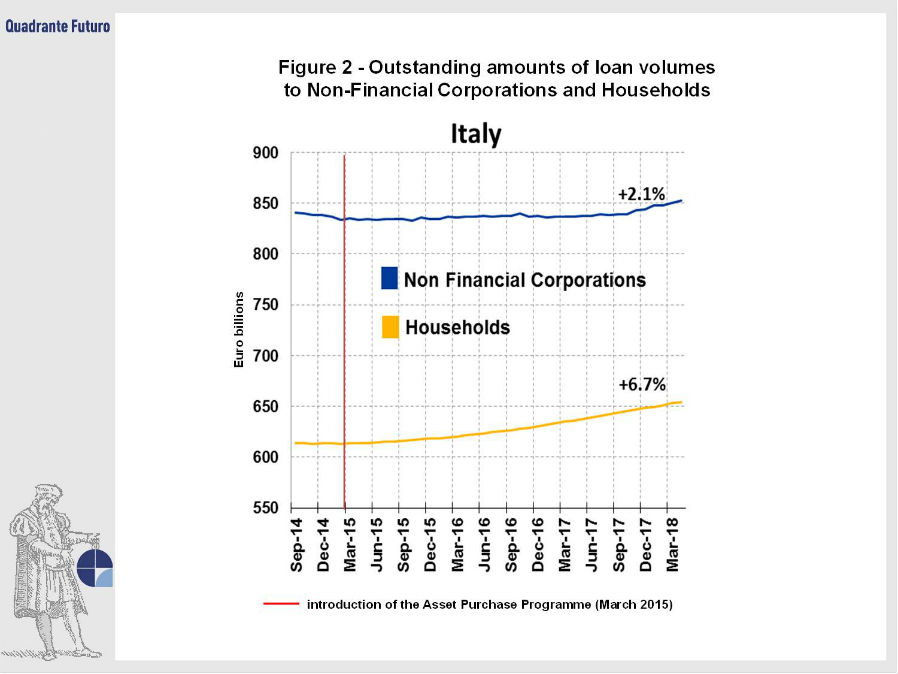

While the increasing pattern for Italian NFCs has been fostered especially in the long term, households volumes of loan growth has been much rapid soon after the implementation of the policy (Figure 2). Overall, we can confirm a rise of 2.1% for firms and 6.65% for families’ volumes, as of the end of April 2018. Not stunning results compared to the +11% and +10% of Germany (Figure 3), but still a valuable result for a country with considerable resistance to economic expansion in the last 10 years. It becomes quite easy to claim that without the programme, probably, Italian credit easing reaction would have been nihil or even negative.

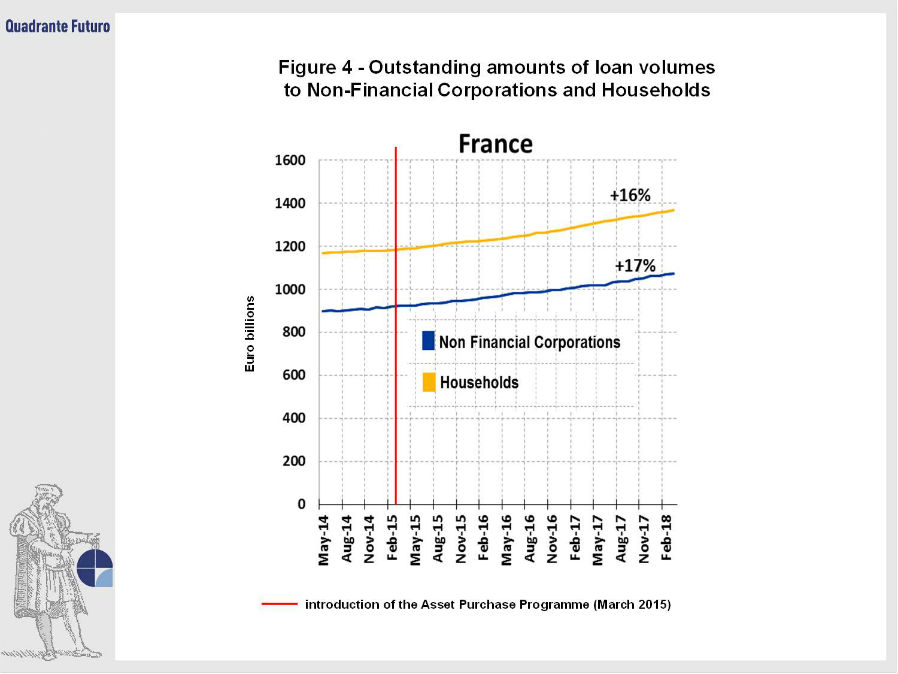

Different results are suggested by the research in France (Figure 4): the considerable confidence of French companies in market funding via corporate bond issuance makes the impact of the policy relatively lower compared to Germany and Italy, at least in the short term.

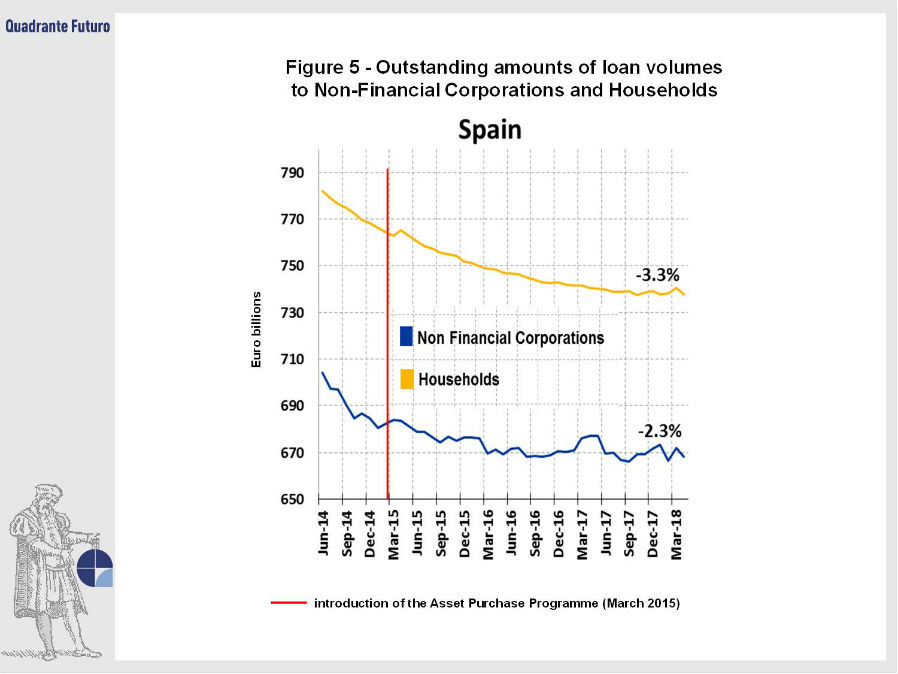

As for Spain (Figure 5), the picture is shaped by the evolution of credit market in the previous years: over-exposure to private debt (NFCs & HHs) between years 2002-2012 imposes to the crushed banking system during the last five years to apply a huge tightness of credit easing. The ESM assistance program started in June 2012 for banking recapitalisation is a confirmation of the adversities of the banking sector. As a result, the favourable liquidity conditions provided to the APP shock were not exploited even though the demand for credit was massively increasing. The sign of a surprisingly weak response of Spanish volumes to the shock in the model is confirmed by the downward trend of the loans since the beginning of the APP, -2.3% and -3.3% for firms and households respectively.

Conclusions

The results of the APP are not to be taken as granted. Overall, it largely contributed to the rebound of the Euro Area economy, which has suffered detrimental economic and financial crises. GDP and especially inflation have reached satisfying numbers at an aggregate level with respect to the main objective of the ECB.

Even though the community authorities (the ECB in this particular case) operate and develop their policies to fulfil the mandate representing all the member countries, it is undeniable that the measures have heterogeneous (partial, at least) effects.

Besides the intent of the empirical analysis, this article does not intend to advocate to the (wrong) belief that the APP was pursued to favour some specific countries, but intends to promote a a reasoning on the universalist approach to policies leading to different effects among distinct economies.

[1] The purchases of new issued money will end in December 2018 with the reduced amount of € 15 bn. However, the reinvestment of the principal payments from maturing securities purchased under the APP will last for an undefined period of time.

[2] Operations conducted for monetary policy purposes for which the APP constitutes the majority in terms of total volumes. Quantitative effect cited in Praet (2018).

[3] The counterfactual analysis carried out in the model of research reveals the net value between the amount found in a model with the introduction of the monetary expansion and one without it. E.g., if the impact of the policy on GDP is very high in the model, does not necessarily mean that the real variable exhibits such a big increase. It can be the case that the GDP is flattening after the policy introduction, but without that, it would have been negative.

Bibliography

Council, E. G. (14 June 2018). Press release - Monetary policy decisions. Frankfurt am Main: ECB.

Musso, A., & Gambetti , L. (June 2017). The macroeconomic impact of the ECB's expanded asset purchase programme (APP). ECB Working Paper Series.

Praet, P. (14 March 2018). Assessment of quantitative easing and challenges of policy normalisation. ECB and Its Watchers XIX Conference. Frankfurt am Main: ECB.

Tozzo, J. (March 2018). Macroeconomic effects of Asset Purchase Programme on Euro Area. A country-level analysis on major economies. Master Thesis (not published).

The charts data source is the public Statistics Data Warehouse of the European Central Bank.

© Riproduzione riservata

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}