Il saldo della bilancia commerciale è un importante indicatore economico: ne analizziamo i più recenti andamenti

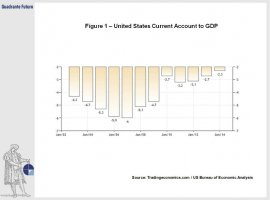

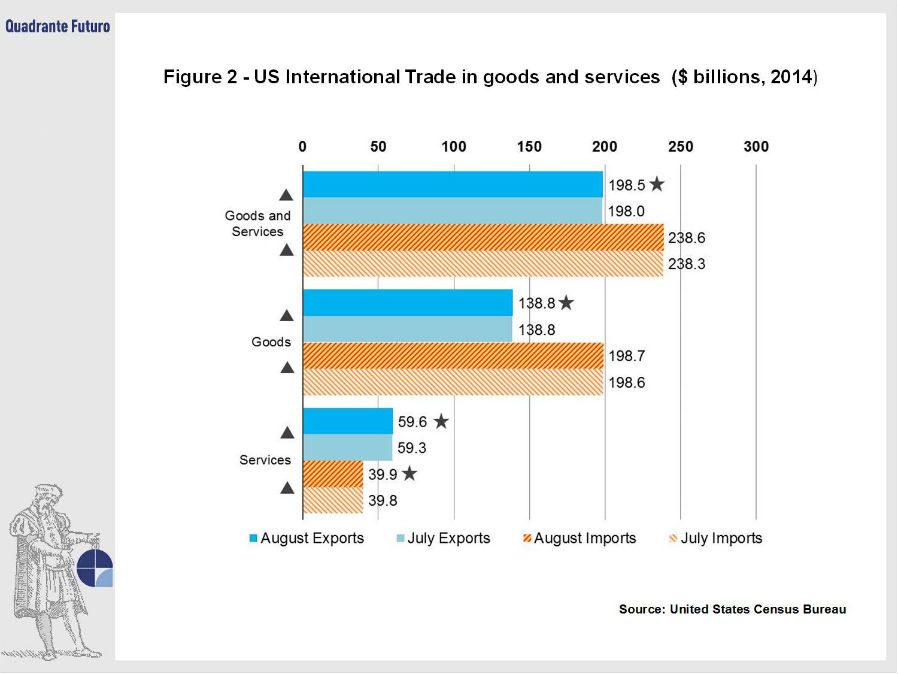

Back in January 2006 the U.S. current-account to GDP ratio reached an alarming level of almost -6%, giving the United States the award of being "the only large industrial country that has run current-account deficits in excess of 5%" (Sebastian Edwards, 2005). According to this author, "never in the history of modern economics has a large industrial country run persistent account deficits of the magnitude posted by the U.S. since 2000" (Figure 1). In January 2014 U.S. current-account deficit narrowed considerably to -2.3% as exports are on the rise. The increase in goods and services exported during the fourth quarter was mainly driven by petroleum and agricultural products. According to the U.S. Census Bureau latest trade highlights, exports in the United States increased to $198,5 billion in August 2014 reaching an all-time high on a 22 year time-frame observed by the institute (Figure 2).

The current-account balance represents an important economic indicator, especially when countries are importing more goods and services than what they export, thus creating a trade deficits and clashes between international economics and politics. The current-account mainly measures the trade of a country, although it also includes net income (such as interest and dividends) and transfers from abroad; additional components which make up only a smaller part of current-account compared to import and exports. This indicator is part of a country's balance of payment and represents the main calculation of a country's foreign transactions. Countries with trade deficits are usually big spenders. The United States and China are the main protagonists of such indicator, as the U.S. was the largest deficit economy in 2006 and China the largest surplus leader in the same year.

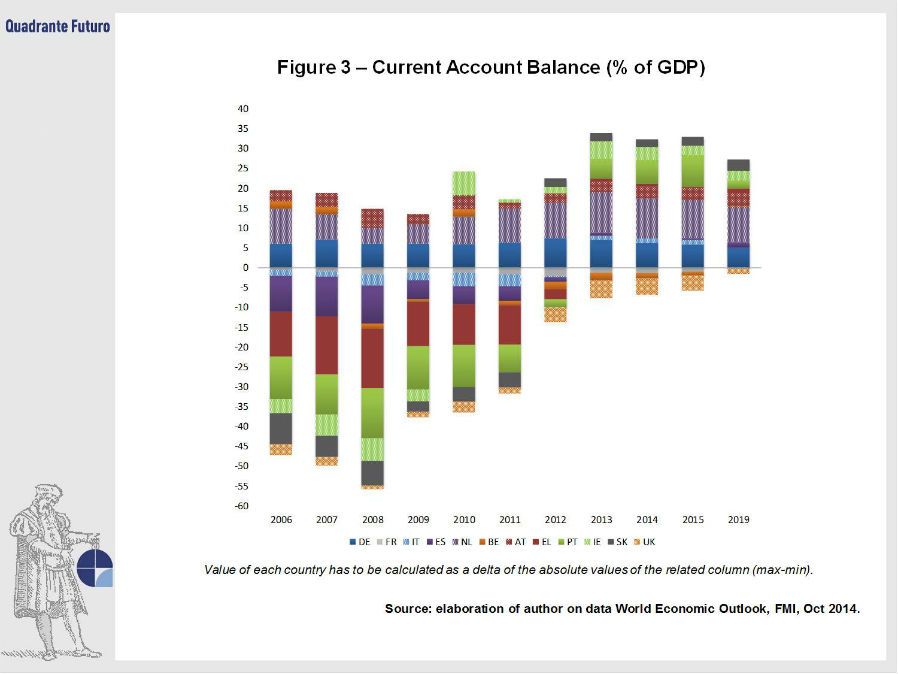

If we look at today's current-account balances, we will see that other countries - especially in the Eurozone - are running substantial deficits. For instance the U.K. stands at -4.2% of GDP in 2014, representing the worst performer among the EU countries taken into consideration (Figure 3). As a per cent of GDP, the current-account deficits of the major European countries peaked in 2006-2008, shrank in 2009 - when the volume and value of global trade declined - and stabilized between 2010 and 2011. However, on the one hand, there are countries like Greece, Spain and Portugal that from 2012 and on show improving data, switching their trends from deficits to surpluses. On the other hand, Germany, Austria and the Netherlands register positive and increasing surpluses, with constant values forecasted for 2015 and 2019. The Italian data reveal a positive balance between 2013-2015, with a 2014 current-account balance of 1.2% of GDP compared to -3.4% in 2010. Among the worst performers stand the UK (-4.5% in 2013, -4.2% in 2014), France - with a deficit of -1.3% in 2013 and -1.4% in 2014 - and Belgium with a trade deficit of -1.9% in 2013 and -1.3% in 2014.

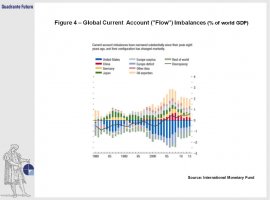

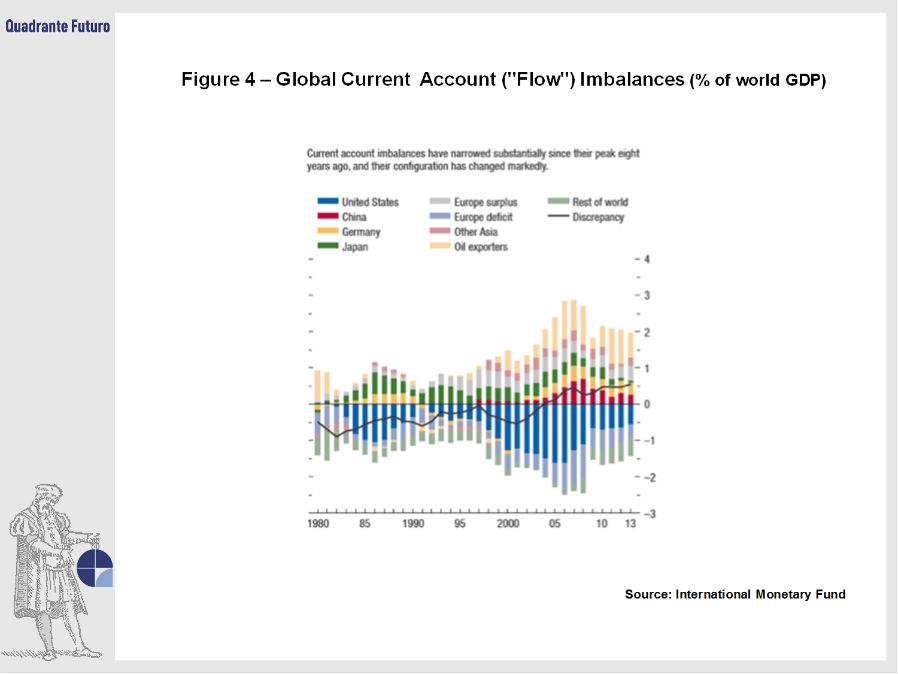

The plunge and renewed surge in commodity prices (especially oil) was one major factor affecting the whole trend. While the balances of the main surplus and deficit countries are below their pre-crisis peak, global imbalances are still under the observation lenses by many economists. On the other hand, the American economist B. Eichengreen (2014) argues that "global imbalances are over because neither the United States (the largest deficit economy in 2006) nor China (the largest surplus economy in 2006) will return to pre-crisis growth and spending patterns" (Figure 4).

Thanks to an energy boom the United States has recently reduced its trade deficit, as a percentage of global GDP, from -3.2% of January 2012 to -2.3% of January 2014. According to Bank of America the U.S. has produced 70% of the energy it consumed in 2008 and since then the value has risen up to almost 90%. Moreover, Americans spend less on imported goods and more on domestic produced services like healthcare, recreation and food. In addition to energy, manufacturing is also showing a coming back. A recent survey made by the Boston Consulting group explains how more than half of the U.S-based manufacturing companies are actively planning to shift the production back to America. Whirlpool, Apple, Ford Motor and General Motors are examples of American manufacturing giants that are restoring nationally the production of some machines. This will in turn increase trade competitiveness and quality, though not the more than 2 million jobs lost during the recession. Therefore, the U.S. deficit is down sharply from the peak of -6% between January 2006-2007, trending near the lowest level in five years (Figure 5).

The current-account deficit can however also express an excess of investments over savings, as it can also measure the difference between national savings and investments. In this case, a deficit can reflect low savings relative to investment or a high rate of investment, or both. Therefore, it is difficult to say whether deficits are good or bad to an economy, because there are different factors causing current-account deficits. However, the debate around global imbalances fired up around the year 2000s when many argued about the causes and consequences of such imbalances, especially referring to the financial crisis. According to A. Greenspan, global imbalances are simply natural events coming from the international integration, which implies that countries can finance their savings-investment unbalance with capital flows coming from abroad. On the other hand, the major assumption is that global imbalances were generated by the recreation of an international monetary system similar to Bretton Woods, in which the United States and China shared the mutual interest of keeping up global imbalances. This mutual decision favored an overvaluation of the Chinese currency, which was needed to finance a surplus of the Chinese domestic demand and in turn to increase the U.S. dollar reserves.

If we look again at the figures proposed in this analysis, we can clearly see a strong reduction of global imbalances, especially for the United States and Europe as well. However, it is still very hard to answer the questions: "Can global imbalances come back? When should we worry?"

© Riproduzione riservata

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}