In occasione dell'Expo 2015 di Milano, è interessante analizzare la situazione dei consumi, della propensione al risparmio e di altri indicatori economici nell'Unione Europea

"Feeding the Planet, Energy for Life", the theme of the World Expo Milano 2015 is of vital importance for Europe in this unsteady climate. Food security and environmental sustainability are some of the world's issues over which Expo Milano 2015 will focus its attention. In the light of this global event (with 19 EU Member States and a total of 147 participating countries) and the European Year of Development (2015), the climate of consumptions in Europe, the willingness to buy, the propensity to save and other economic indicators are under crucial examination.

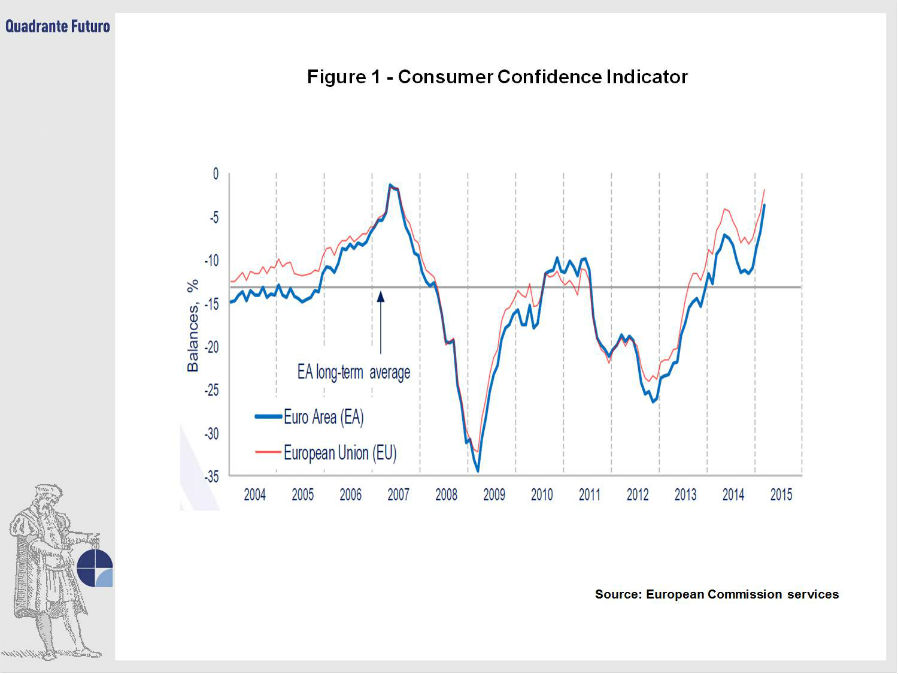

According to the latest releases, the consumer climate and the economic expectations in Europe are forecasted to have a brighter outlook with few cloudy conditions. The Business and Consumer Surveys of the European Commission show an upswing for the current year and a positive improvement in consumers' confidence, which encourage European households and individuals to spend more (Figure 1). In March 2015 the increase in consumer sentiment in the EU is revealed by a rise of 2.6 points from the negative 1.8 of the previous month. The same indicator jumped from -3.7 of February 2015 to a positive 3.0 of March in the euro area. Such bright responses arise from the positive estimates on unemployment data and an optimistic prospect on the general European economic outlook.

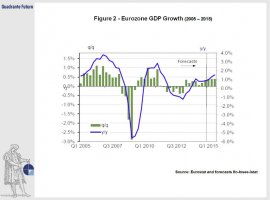

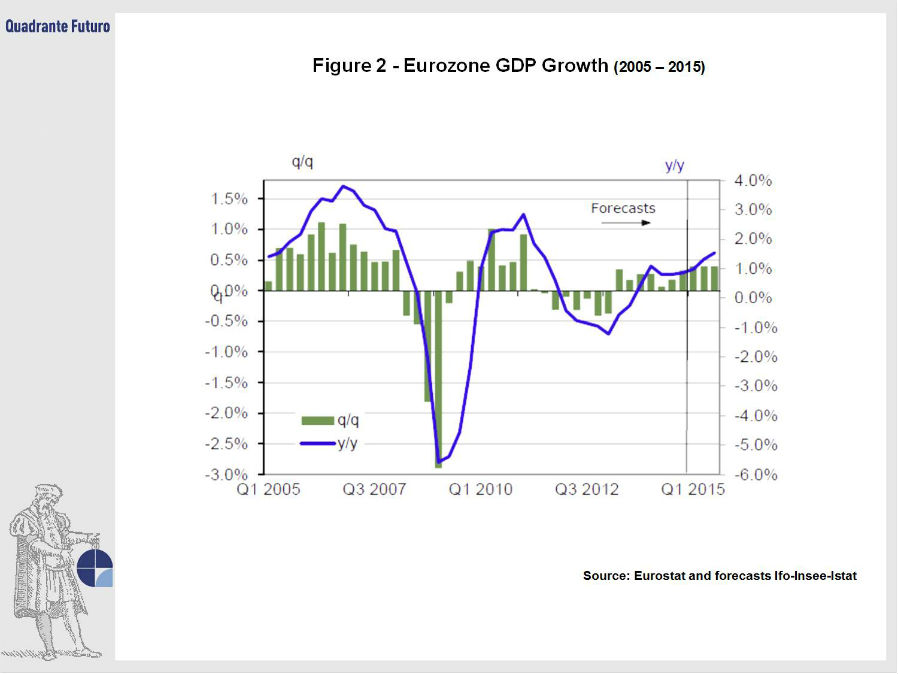

The Eurozone is experiencing a steady recovery from the financial and economic crisis, considering that the economy is moderately picking up at different speeds across the member states. The GDP grew from 0.2% in Q3 of 2014 to 0.3% in Q4, and data are showing a further speed up in Q1 of 2015 to 0.4%, which is continuing to expand – at about the same pace – in the following quarters (Figure 2).

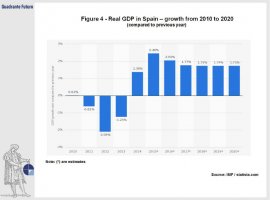

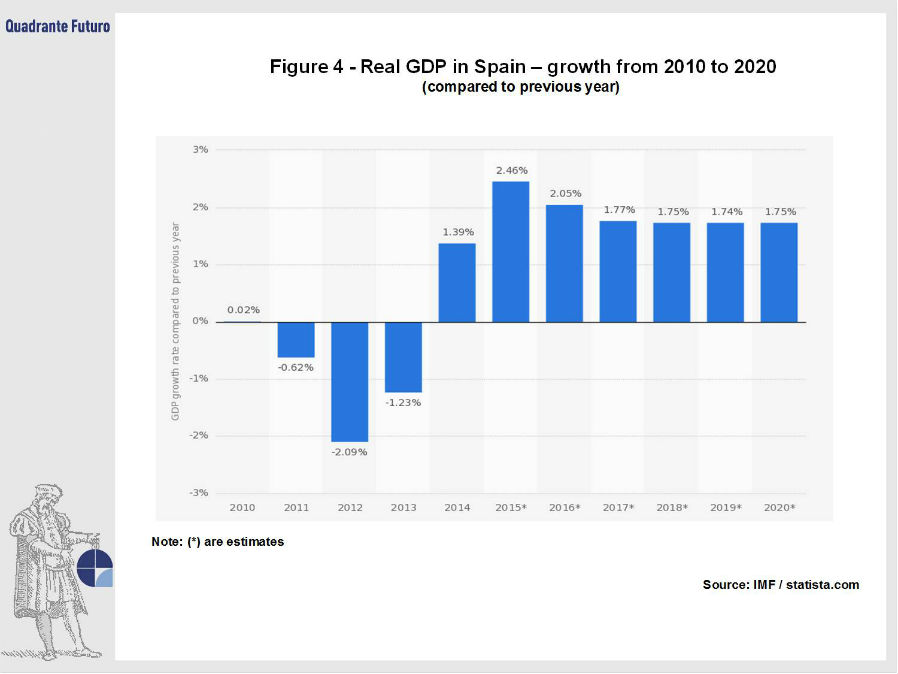

On one hand, the upswing experienced in Q1 of 2015 was encouraged by the depreciation of the Euro and the fall in oil prices (at around $57 a barrel at the end of April 2015), which can be translated in lower costs for consumers in importing countries and thus an increase of income for households and firms. On the other hand, the Eurozone growth was pushed by the unexpected strong upturn of the German economy (GDP is forecasted to increase by 2.1% this year) and by other contributors such as Spain, which showed a 1.39% increase in real GDP in 2014 and an estimated rise of 2.46% in 2015 (Figure 3 and Figure 4).

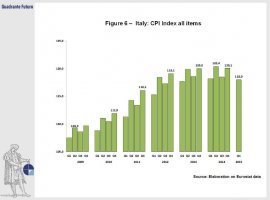

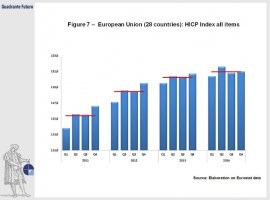

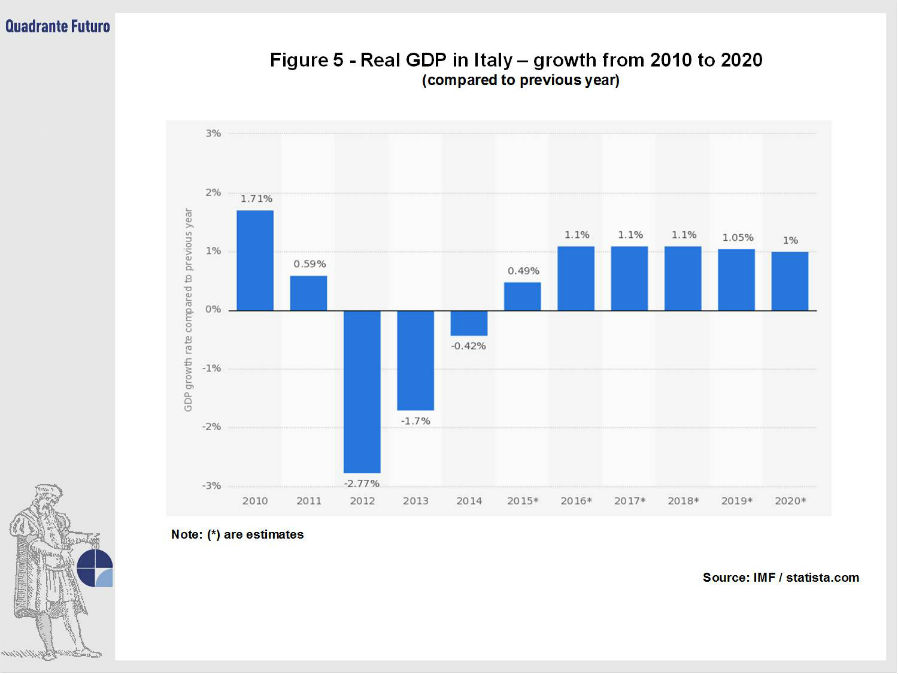

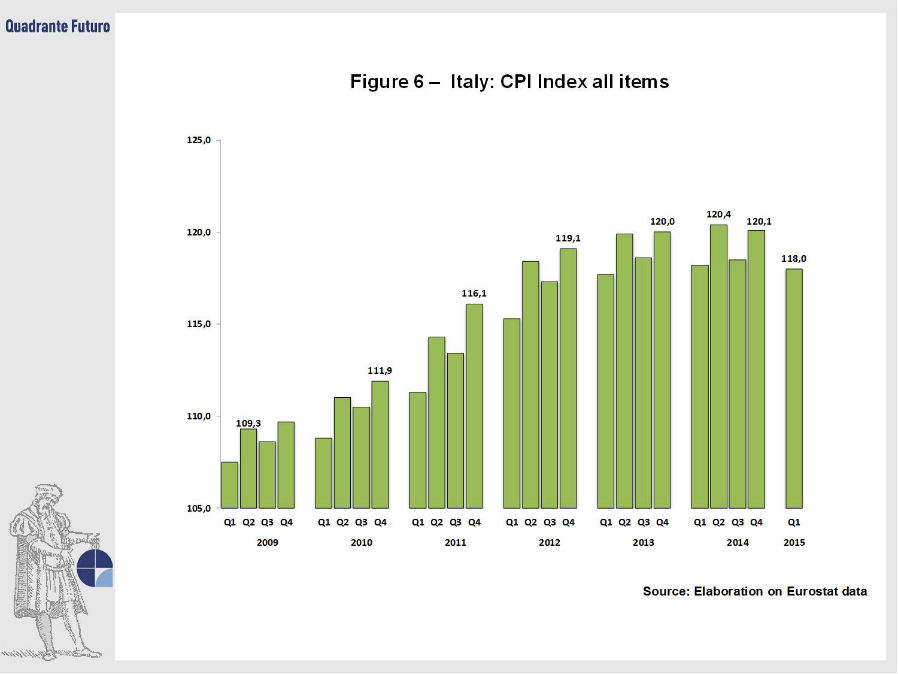

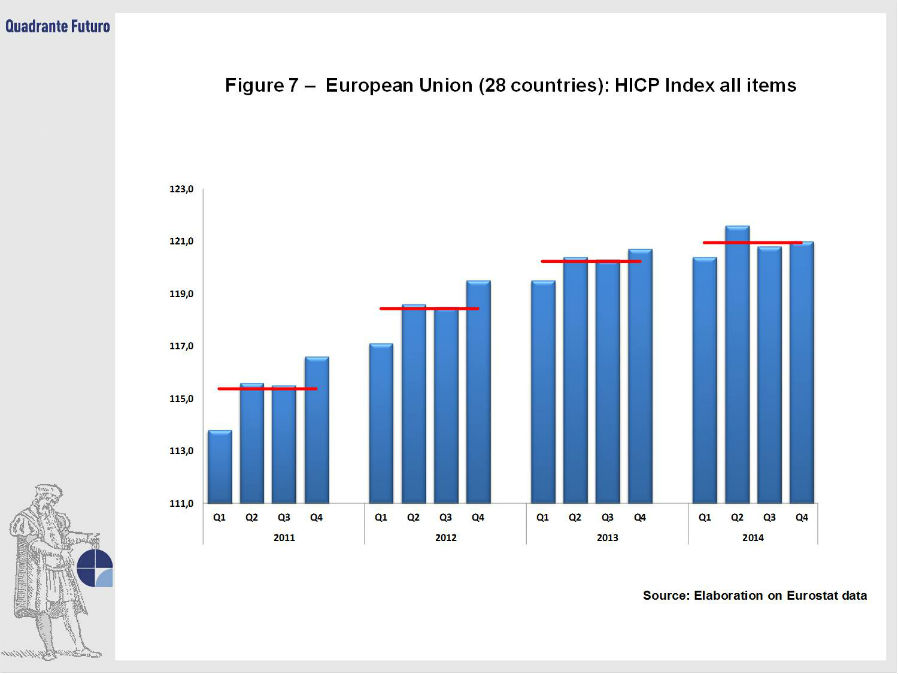

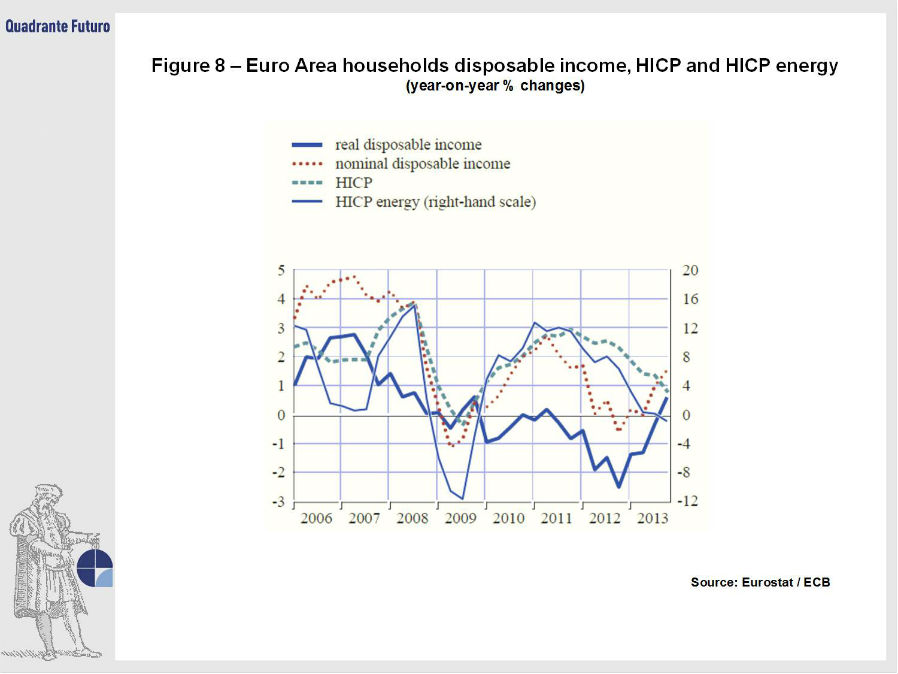

Recent data confirmed a modest improvement of the Italian economy, with positive sentiments coming from households' conditions. Growth was forecasted at a positive 0.5% for 2015, unlike 2014, while estimates for 2016 are even brighter with 1.1% real GDP forecast (Figure 5). The consumer price index (CPI) related to all items jumped from its lowest 107.5 points in Q1 of 2009 to its highest 118.2 Q1 of 2014. Recent estimates show a similar trend also for Q1 of 2015 with 118 points (Figure 6). Overall, the European consumption showed a positive climate for 2014 with the harmonized index of consumer prices (HICP) at its highest (121.6) in the second quarter (Figure 7). Moreover, the CPI in EU28 increased to 120.9 index points in March 2015 from 119.8 of February 2015, while for the Eurozone (19 member states) the indicator increased to 118.1 in March 2015 from a lower 116.8 of the month before. These evidences are highlighted by the improvement of consumer's real disposable income, their willingness to buy and the positive signs coming from the labor market (Figure 8). However, the heterogeneous features of the Eurozone countries reveal the uncertain trend of some member states.

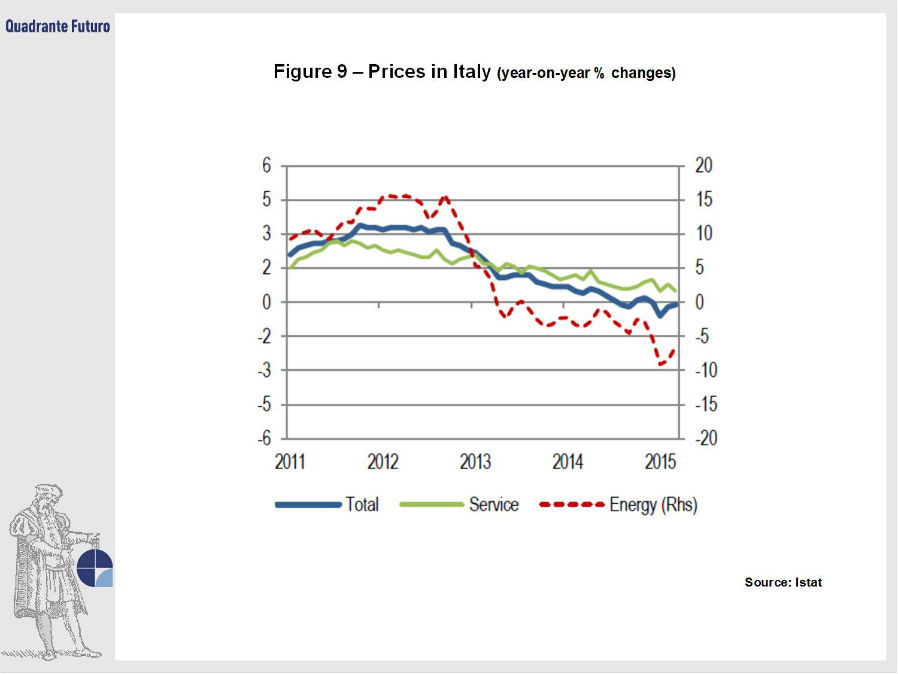

The harmonized index of consumer prices (HICP), also called CPI, is the barometer used to compare inflation rates among European countries, and a key element to take into account when deciding the monetary policy of a member state. The Italian inflation rate was negative – for the third time – in March, standing at -0.1%.

The largest downward pressures are coming from the energy and the service sector, which slowed down the core inflation to 0.4% (Figure 9).

The consumptions composition is showing encouraging trends in some of the most important European countries (Italy, France, Germany and United Kingdom) over the last 8 years, from 2005 to 2014. The observed sectors are: food, health, education, recreation & culture, household equipment and transport. According to the data, the Italian economy is registering a positive recovery in food, health, education and transport between 2010 and 2014. Moreover, France and the UK are showing a peak in education during the last three years, denoting that consumers are heavily investing in schooling. In most countries, the weight change of these sectors is highlighting a steady upturn from the economic and financial crisis, with the exemptions of Germany's education sector and France's recreation & culture sector (Figure 10).

It is moreover interesting to notice that, according to CPI data, the index on food and non-alcoholic beverages consumption in Italy and overall in Europe is showing an increasing trend. The index related to Italy increased to 121.3 points in Q1 of 2014 with respect to 120.4 in Q1 of 2013 and 117.5 points of 2012. The same positive mood is reflected also for EU28 with 126.5 index points in Q1 of 2014 from 121.7 of 2012, and 118 points in 2011 (Figure 11). After more than four years of declines and unsteady pace, both household disposable income and consumer's confidence are moderately picking up and forecasting an optimistic climate for Europeans.

© Riproduzione riservata

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}